Award-winning PDF software

Form Schedule K-1 (1065-B) for Montgomery Maryland: What You Should Know

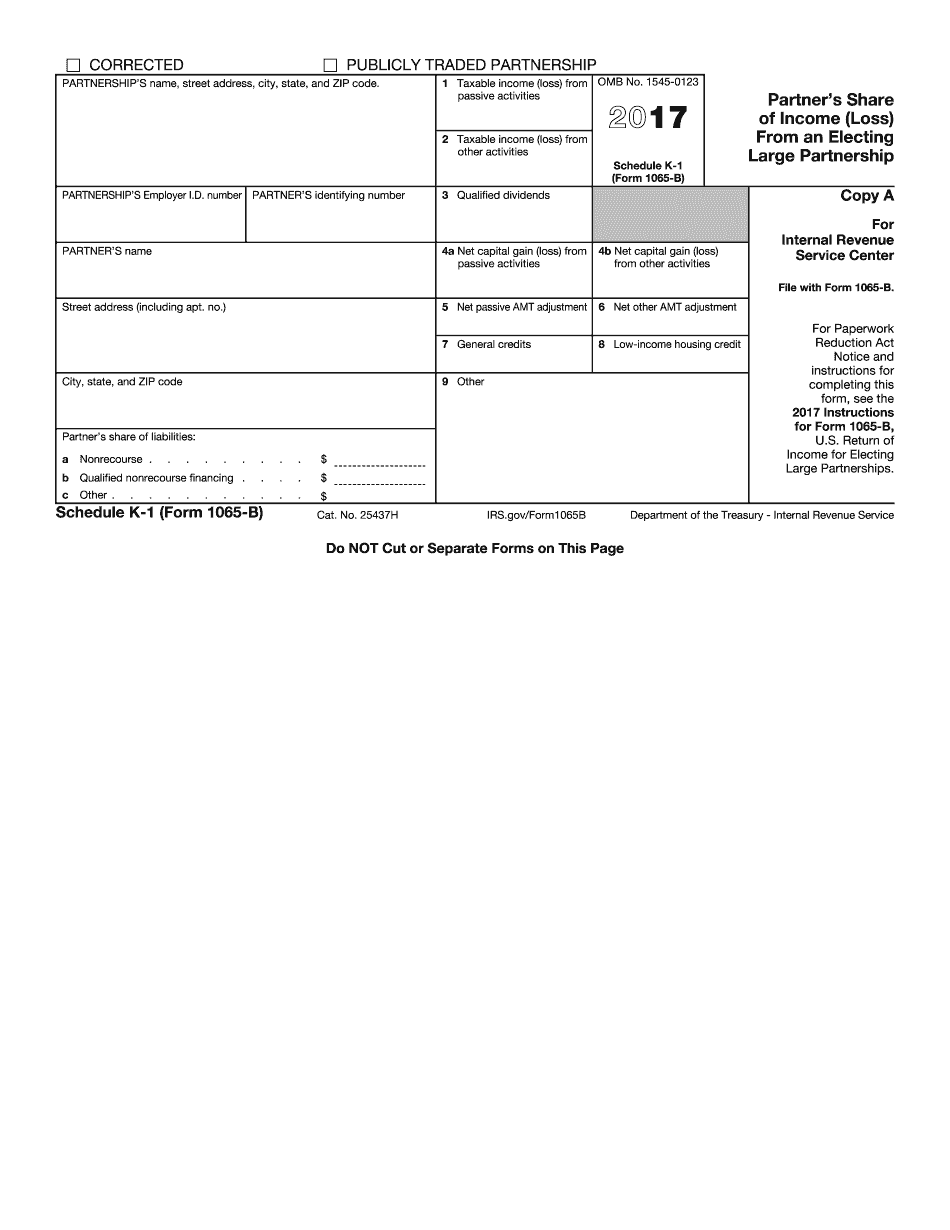

The form must be filed by partnership members to report the income and deductions related to the partnership. For tax year 2018, a partner's gross income is determined on lines 30, 31, and 32. The partner's net income is determined on lines 6, 7, and 8. For tax year 2017, a partner's gross income is determined on lines 30, 31, and 32. The partner's net income is determined on lines 6, 7, 8, and 9. For tax year 2016, a partner's gross income is determined on lines 30, 31, and 32. The partner's net income is determined on lines 6, 7, 8, and 9. For tax year 2015, a partner's gross income is determined on lines 30 and 31. The partner's net income is determined on lines 6 and 7. The partner's basic withholding and reporting is described in section 743 of Internal Revenue Code (IRC) Sections 6652(m)(1)-(3).” “The basic income and withholding from your partnership income does not differ substantially from the basic withholding and reporting on Forms W-2 you pay to employees. This means that the partnership tax is not withheld from gross income received by partners. However, certain partnership tax provisions are still imposed at the partnership level.” “If you are self-employed and the partnership is not in a business with the self-employed for profit or gain, then the tax on partnership returns does not apply.” The income attributable to pass-through or Fiduciary income is not reportable to partners, as described in IRC Sections 1.199-21(a)(2) and 1.199-21(a)(4) and (c).” “For purposes of IRC Sec. 1.199-21(a)(4), a partnership or an S corporation is “in business with the self-employed for profit or gain” if, because of the business of the entity, the entity generates gross income from a trade or business.” “A reportable partnership includes any partnership (including the partnership referred to in section 743(a)(7)) with one or more partner(s) which meets all the other criteria described in that section.” “Any trust or trust company described in section 771 must be treated like an S corporation for the purpose of tax treatment under sections 771 and 877.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form Schedule K-1 (1065-B) for Montgomery Maryland, keep away from glitches and furnish it inside a timely method:

How to complete a Form Schedule K-1 (1065-B) for Montgomery Maryland?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form Schedule K-1 (1065-B) for Montgomery Maryland aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form Schedule K-1 (1065-B) for Montgomery Maryland from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.